Business

Tariff Squeeze: How Pennsylvania Car Insurance Could Rise

Tariffs on imported auto parts don’t just affect dealership sticker prices—they ripple through collision shops, supply chains, and ultimately the premiums Pennsylvania drivers pay every renewal. New projections suggest that, by late 2025, rates in the Commonwealth could end up higher with tariffs than without them as parts inflation and longer repair times push claim costs up. If you drive in Pittsburgh, Philly, Erie, or anywhere in between, now is the time to get proactive: line up quotes, right‑size coverages, and use competition to your advantage. This guide breaks down what’s changing, why it matters, and the concrete steps to protect your wallet without hollowing out your protection.

What the latest projections show

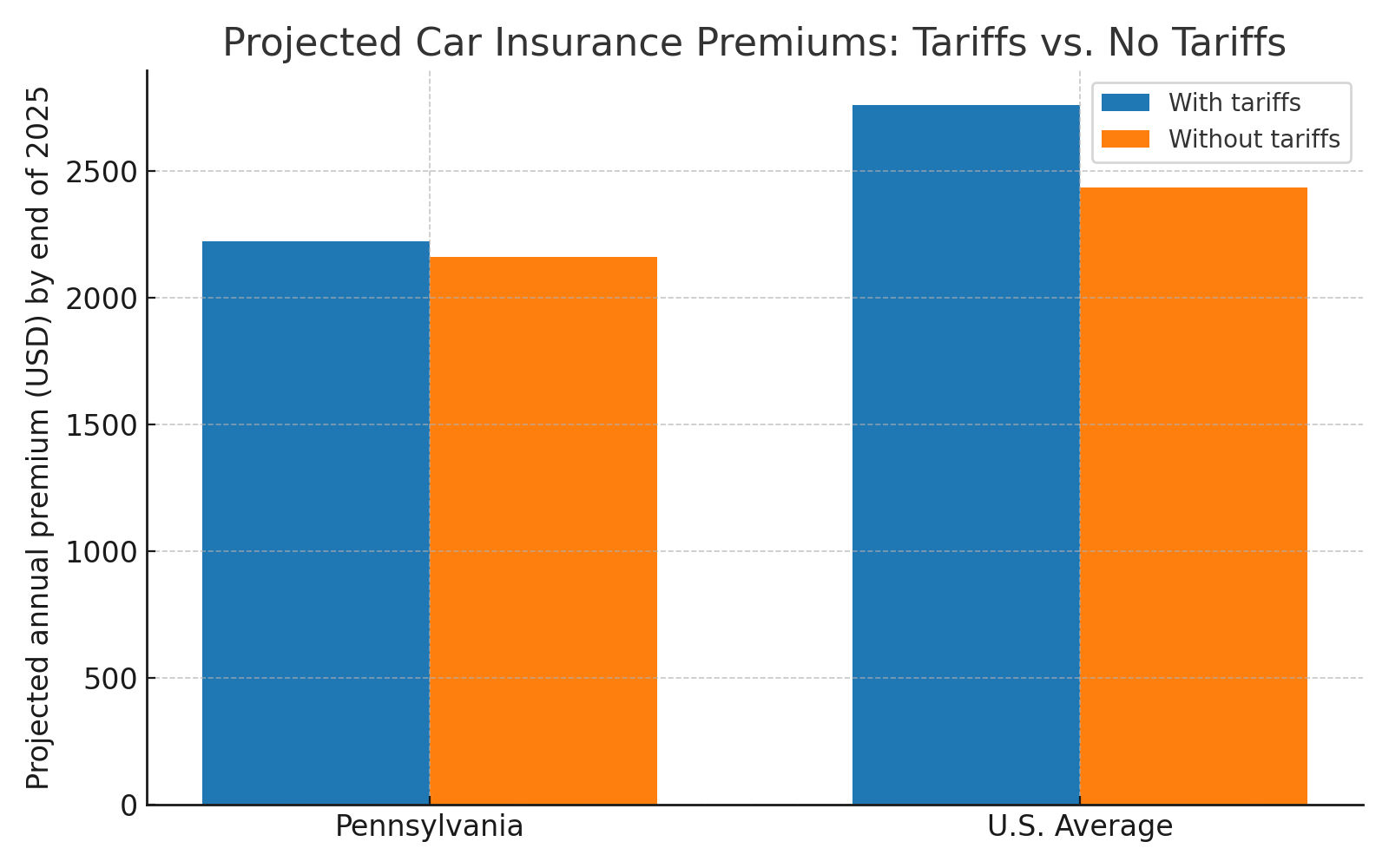

Analyses cited by regional and national outlets indicate that car insurance could rise more with tariffs than without them. For Pennsylvania specifically, recent reporting points to a scenario in which average full‑coverage premiums land around the low $2,200s with tariffs by year‑end, versus roughly the low $2,100s without. The exact number you pay will depend on your record, vehicle, and ZIP code, but the directional takeaway is clear: parts‑price pressure and supply‑chain friction can lift insurers’ claim costs—and premiums follow.

Illustrative end‑of‑2025 premium scenarios

| Region | With Tariffs (illustrative) | Without Tariffs (illustrative) |

| Pennsylvania — full coverage | $2,223 | $2,160 |

| United States — full coverage average | $2,472–$2,759 | $2,402–$2,437 |

Note: Ranges based on recent reporting and public projections; your rate will vary by driver profile, carrier, and policy form.

How tariffs translate into premiums (in plain English)

- Imported parts get pricier: Bumpers, cameras, radar sensors, and EV body panels subject to new duties cost more. Those components now dominate repair bills, especially on late‑model vehicles with ADAS.

- Repairs stretch longer: When suppliers reprice and inventory tightens, cycle times increase—extending rental‑car days and labor hours.

- Claim severity climbs: Higher parts and labor lift the average cost per claim. If total‑loss thresholds are reached sooner, payouts rise as well.

- Insurers refile rates: Actuaries price for expected losses. If severity trends higher than assumed, carriers seek adjustments at renewal.

Who is most exposed in Pennsylvania

- Urban commuters in dense corridors (Pittsburgh/Allegheny County, Philadelphia, Montgomery/Delaware counties).

- Owners of late‑model vehicles with complex driver‑assistance tech (costly sensors, calibration).

- Households with youthful drivers or recent at‑fault claims/violations.

- Drivers parking on‑street in theft‑prone ZIP codes (comprehensive premiums stay elevated).

Action plan: 9 steps to blunt tariff‑driven increases

- Start quotes 30–45 days before renewal so you can compare calmly—not the week your bill arrives.

- Quote 5+ carriers, including at least one regional or mutual; appetite varies by ZIP, vehicle, and mileage.

- Try a 60–90 day telematics trial; if your score is favorable, keep it for renewal savings.

- Set deductibles where savings justify risk (e.g., moving from $500 to $1,000); avoid extremes if cash reserves are thin.

- Bundle home/renters with auto and audit all discounts (advanced safety, verified mileage, defensive‑driving course).

- Review liability limits and uninsured/underinsured motorist (UM/UIM); use any savings to strengthen protection.

- Ask your body shop about OEM vs. aftermarket parts; knowing the difference helps you compare carriers’ parts language.

- Check glass coverage and calibration rules for ADAS windshields—costly surprises can be avoided with the right endorsement.

- If your vehicle is older and paid off, weigh whether comprehensive/collision still passes a cost‑benefit test.

Choosing a financially sound carrier

Financial strength, claim handling, and underwriting appetite matter more when costs are volatile. For a practical checklist on comparing insurers (AM Best ratings, complaint ratios, claim service, and discounts), read: how to pick the right auto insurance company

If you pay attention to how insurers and regulators talk about these trends, you’ll get better at reading filings and policy forms. A quick explainer on how the language evolves—what terms like “severity,” “combined ratio,” or “cat loss” signal—can help you shop smarter: auto insurance word trends and insights

Quick wins vs. risky cuts

| Quick Wins (keep protection strong) | Risky Cuts (could backfire) |

| Shop multi‑carrier quotes and keep a favorable telematics program. | Dropping UM/UIM or medical benefits to save a few dollars. |

| Bundle policies; verify ADAS, mileage, and homeowner discounts. | Cutting liability limits below what you’d need to protect assets/income. |

| Increase deductibles modestly to target diminishing‑return premiums. | Removing comp/collision on vehicles you can’t afford to replace. |

Fast FAQ for Pennsylvania drivers

Will every driver see increases?

No. Pricing is individualized. Clean records, low annual miles, and garaging in lower‑risk ZIPs can still produce flat or lower renewals.

When would changes show up?

Most carriers phase adjustments at renewal. Timing differs by company and filing approval date.

Can switching carriers hurt me later?

Not if you maintain continuous coverage and avoid short policy terms. Keep proof of prior insurance to qualify for longevity discounts.

Are aftermarket parts always cheaper?

Often, yes—but not always after tariffs. Availability and calibration requirements can change the math. Ask the shop and your carrier.

Is minimum coverage a smart way to save?

Usually not. A single serious crash can exceed state minimums. Use shopping and discounts to keep strong limits affordable.

Sources & methodology note

This article synthesizes recent reporting on tariff impacts to auto insurance, including Axios Pittsburgh’s coverage of Pennsylvania‑level projections and national projections based on Insurify data. It also references industry commentary on how parts prices and repair cycle times influence claim severity and rate filings. Figures provided here are illustrative and may change as tariffs and insurer filings evolve.

University of Houston graduate with 5 years of blogging experience, excelling in content strategy, SEO, and audience engagement. Connect with me on LinkedIn.